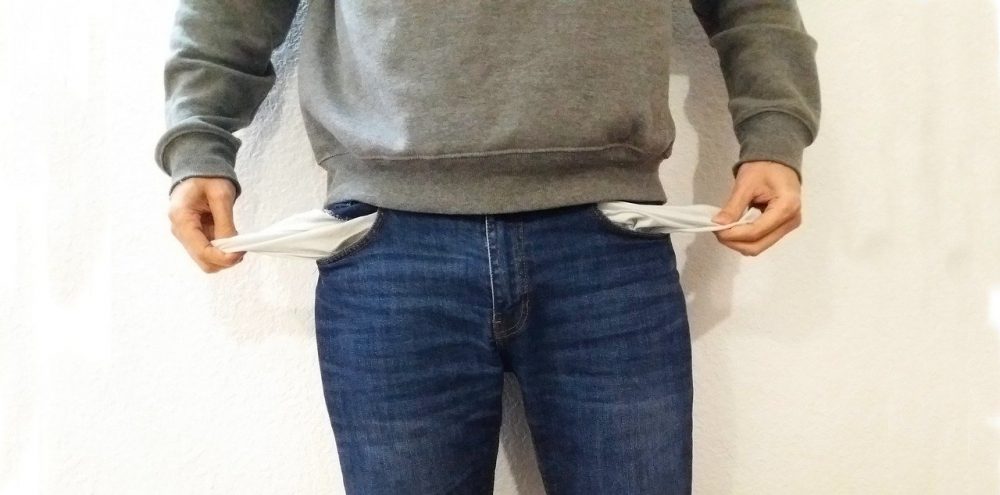

If you’d love a debt consolidation loan to get rid of high-interest debt, don’t give up on the idea just because your credit is poor. There are steps you can take to both improve your chances and get you a better interest rate.

What Is Debt Consolidation?

It’s the process of taking out a new loan to erase other obligations. Multiple debts are combined into a single, larger loan, usually with more favorable payoff terms including a lower interest rate, lower monthly payment, or both.

Borrowers with a FICO credit score of less than 640, however, will likely need to work harder to qualify for a loan. The fact is, finding a debt consolidation loan with bad credit is doable, but you’ll need to put in the effort.

What Can I Do To Help Myself?

Before looking for debt consolidation loan lenders for bad credit, try cleaning up your credit profile. After all, you want to see what creditors see when they look you up.

After getting a copy of your credit report, examine it to see exactly why your score is low. For instance, a lender will look askance at a past-due account, but you’ll have a better chance of qualifying if you see it first and do something about it.

Lenders also factor in your debt-to-income ratio — the percentage of your monthly income that goes toward payments. They usually like to see a ratio of below 50 percent, and the lower the better.

If you don’t need the loan immediately, try to pay down debt before you apply. If you need consolidation right away, consider adding a co-signer who has good credit and a strong income. Careful, though, since the person who agrees to help you out will be liable for the loan if you default.

You should also put together a repayment plan. Lenders report to credit bureaus both on-time and missed payments, so your ability to make your payments will determine the shape of your credit.

Furthermore, understanding a lender’s rates, terms, and extra fees will assure that you know exactly what you will owe each month and when you will owe it.

Still, something may come up and you may miss a payment or two. Because lenders don’t immediately alert delinquent payments to credit bureaus, make the payment as soon as possible to avoid a credit hit.

Compare Lenders

Sizing up offers from credit unions, banks, and online lenders can help you pinpoint the best rate and features for you.

There are lenders that cater to borrowers with low credit scores. Seek out reputable ones that cap their annual percentage rates (APRs) at 36 percent — about the highest rate a manageable loan can carry.

Many online lenders will also let you prequalify for a loan without hurting your credit score. This involves conducting a soft credit inquiry to estimate your likely terms. By contrast, many credit unions and banks require you to officially apply before any offer, prompting a hard check that can cause a temporary drop in your score.

Also, your local credit union or bank may be more amenable to working with you if a recent misunderstanding or long-ago issue has been a drag on your credit.

Note, too, that while an online lender may be convenient and have the most competitive rates, it’s still all about algorithms. Your local institution may be more apt to assess the borrower from a holistic point of view.

So, now that you know how to find a debt consolidation loan with bad credit, you are well on your way to a future of renewed financial stability.

cheap lasuna generic – lasuna over the counter himcolin buy online

order besivance – order carbocysteine without prescription cheap generic sildamax

gabapentin cost – buy sulfasalazine cheap buy sulfasalazine 500 mg generic

order probalan for sale – generic monograph 600mg buy generic carbamazepine

order celebrex 100mg without prescription – flavoxate for sale buy generic indomethacin

colospa 135 mg sale – arcoxia ca purchase pletal

Car Insurance in Las Vegas Nevada is essential

for covering prospective damages and liabilities while driving.

Shopping around may help you locate the ideal fees for Car Insurance in Las Vegas

Nevada. Some insurance carriers use discount rates for bundling Car Insurance in Las

Vegas Nevada with various other policies. It is actually important to

read the fine print of any sort of Car Insurance in Las Vegas Nevada plan to recognize

what is actually covered.

order generic cambia – buy generic cambia over the counter aspirin 75 mg brand

rumalaya where to buy – order elavil pill buy endep without prescription

oral mestinon 60 mg – azathioprine price azathioprine over the counter

cheap diclofenac pills – imdur 20mg usa purchase nimodipine generic

lioresal over the counter – piroxicam buy online piroxicam 20mg drug

order mobic generic – toradol price where can i buy toradol

periactin 4 mg pills – buy tizanidine generic tizanidine tablet

where can i buy artane – emulgel where to purchase buy diclofenac gel online

Lots of motorists are actually going with Cheap car insurance in Indiana to help lesser

their fees. Indiana possesses several companies that supply inexpensive

plans for Cheap car insurance in Indiana.

It is actually vital to contrast quotes to locate the very best costs for Cheap car insurance in Indiana.

Along with the appropriate company, you can easily find Cheap car insurance in Indiana that delivers wonderful

coverage at an affordable cost.

order omnicef 300mg pills – buy generic cleocin online buy generic clindamycin

deltasone drug – zovirax without prescription permethrin creams

oral acticin – acticin without prescription retin cream over the counter

Commercial Van insurance assists you steer clear of out-of-pocket costs in the event that of a

collision. This monetary protection is vital for business that rely upon their trucks.

betamethasone 20gm cost – monobenzone without prescription buy benoquin

buy metronidazole 400mg online – buy cenforce 50mg generic buy generic cenforce for sale

buy generic augmentin online – order synthroid 75mcg generic purchase levoxyl generic

buy losartan 25mg pills – buy keflex 125mg buy generic keflex online

buy modafinil 100mg without prescription – buy generic promethazine buy melatonin 3 mg generic

order xeloda 500mg sale – generic mefenamic acid danazol medication

norethindrone 5 mg price – purchase yasmin sale purchase yasmin sale

fosamax ca – buy provera 5mg pills medroxyprogesterone oral

buy estrace cheap – purchase femara for sale order arimidex 1mg

Drivers in Wisconsin might discover the cost of SR22 Insurance frightening, yet there are actually budget friendly choices.

Taking the opportunity to compare different carriers can lead in considerable savings.

バイアグラは薬局で買える? – タダラフィル処方 タダラフィル処方

гѓ—гѓ¬гѓ‰гѓ‹гѓігЃ®йЈІгЃїж–№гЃЁеЉ№жћњ – гѓ—гѓ¬гѓ‰гѓ‹гѓігЃ®йЈІгЃїж–№гЃЁеЉ№жћњ イソトレチノイン通販で買えますか

eriacta grunt – apcalis fortune forzest goose

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

indinavir for sale – indinavir buy online purchase voltaren gel cheap

valif online party – sustiva 20mg without prescription sinemet online buy

generic ivermectin – atacand 16mg sale tegretol 400mg for sale

promethazine over the counter – lincomycin online order buy generic lincomycin

order deltasone 10mg online cheap – buy prednisone 10mg generic captopril uk

buy prednisone 40mg – cost prednisone 10mg cheap capoten

accutane 40mg generic – dexamethasone 0,5 mg us order linezolid 600 mg generic

order amoxicillin sale – combivent 100 mcg pills buy ipratropium sale

order zithromax 250mg online cheap – purchase tinidazole for sale order nebivolol 5mg sale

generic omnacortil 5mg – generic prometrium prometrium online order

purchase neurontin online – order sporanox 100mg without prescription order itraconazole pill

order furosemide 100mg pills – buy furosemide 100mg betamethasone 20gm oral

clavulanate without prescription – order ketoconazole buy cheap generic duloxetine

monodox pills – cheap monodox buy glucotrol generic

augmentin 625mg cheap – cymbalta 20mg generic oral duloxetine

cost semaglutide – semaglutide 14mg cheap buy periactin medication

buy tizanidine no prescription – tizanidine over the counter microzide 25mg sale

tadalafil 5mg generic – cialis 5mg for sale viagra 25mg

buy viagra 50mg online – cheap sildenafil for sale cialis 20mg ca

atorvastatin 10mg usa – amlodipine pills lisinopril 5mg over the counter

cenforce 50mg price – cenforce cheap buy glucophage 1000mg

generic prilosec – buy tenormin generic buy generic atenolol for sale

order generic medrol – buy aristocort medication cheap triamcinolone 4mg

cytotec 200mcg brand – xenical 120mg price diltiazem without prescription

acyclovir 800mg ca – zyloprim 300mg us rosuvastatin 10mg generic

buy domperidone pills for sale – cyclobenzaprine 15mg pills cyclobenzaprine for sale online

motilium pill – purchase sumycin for sale order cyclobenzaprine 15mg generic

I am really impressed together with your writing abilities and also with the layout on your weblog. Is this a paid subject or did you modify it yourself? Either way stay up the nice quality writing, it is uncommon to look a great blog like this one today!

order inderal sale – order plavix for sale order generic methotrexate 10mg

cost warfarin 5mg – buy coumadin generic cost cozaar

buy generic levaquin 500mg – buy cheap ranitidine order zantac 150mg

purchase esomeprazole generic – imitrex oral sumatriptan online buy

mobic 7.5mg for sale – celebrex usa oral flomax 0.4mg

купить аккаунт площадка для продажи аккаунтов

покупка аккаунтов безопасная сделка аккаунтов

продажа аккаунтов соцсетей магазин аккаунтов социальных сетей

Mild to moderate ED in aging men is commonly treated with oral agents like viagra generic. Discreet today, unforgettable tomorrow.

платформа для покупки аккаунтов маркетплейс аккаунтов соцсетей

покупка аккаунтов купить аккаунт

биржа аккаунтов магазин аккаунтов

маркетплейс аккаунтов купить аккаунт

маркетплейс аккаунтов маркетплейс аккаунтов соцсетей

маркетплейс для реселлеров продажа аккаунтов соцсетей

маркетплейс для реселлеров услуги по продаже аккаунтов

безопасная сделка аккаунтов аккаунт для рекламы

заработок на аккаунтах маркетплейс аккаунтов

маркетплейс аккаунтов соцсетей https://ploshadka-prodazha-akkauntov.ru/

маркетплейс аккаунтов профиль с подписчиками

услуги по продаже аккаунтов https://kupit-akkaunt-top.ru/

профиль с подписчиками https://pokupka-akkauntov-online.ru/

Secure Account Purchasing Platform Accounts market

Account Buying Platform https://accountsmarketplacepro.com

Secure Account Sales Social media account marketplace

Buy Account Sell accounts

Profitable Account Sales Account trading platform

Accounts for Sale Sell accounts

Account Buying Platform Account Exchange Service

Account Trading Account Exchange Service

Marketplace for Ready-Made Accounts Buy Pre-made Account

Account trading platform Account Selling Platform

Online Account Store Account Acquisition

database of accounts for sale https://bestaccountsstore.com

account selling platform https://cheapaccountsmarket.com

account market marketplace for ready-made accounts

marketplace for ready-made accounts https://buyaccountsdiscount.com/

database of accounts for sale sell account

gaming account marketplace secure account purchasing platform

gaming account marketplace account trading

sell account account marketplace

buy account buy pre-made account

sell account account trading service

website for selling accounts website for selling accounts

secure account sales website for buying accounts

website for selling accounts account market

accounts market account acquisition

account store accounts for sale

account selling service ready-made accounts for sale

account trading platform verified accounts for sale

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

account market ready-made accounts for sale

account exchange service account catalog

accounts for sale buy and sell accounts

accounts marketplace https://marketplace-social-accounts.org/

marketplace for ready-made accounts accounts marketplace

account selling platform secure account sales

account exchange service account buying service

website for buying accounts purchase ready-made accounts

account purchase account exchange service

account exchange find accounts for sale

account store account market

buy pre-made account https://accounts-offer.org/

Присоединяйтесь к нашему сообществу в Курске и найдите девушку на любой вкус. Здесь как минимум несколько личностей ждут, чтобы стать не только праздничным дополнением, но и настоящими участниками вашего досуга. Откройте новые грани общения и веселья https://t.me/kursk_girl_indi

account exchange service https://accounts-marketplace.xyz

online account store https://buy-best-accounts.org

Найди свою девушку из Краснодара среди множества реальных анкет и начни общение уже сегодня https://krasnodar-girl.life/

buy account https://social-accounts-marketplaces.live

account exchange https://accounts-marketplace.live/

account marketplace https://social-accounts-marketplace.xyz

online account store accounts marketplace

gaming account marketplace https://buy-accounts-shop.pro/

Smoking and inactivity contribute to vascular issues that interfere with response to viagra 100mg. Feel confident knowing your order travels safely through normal post.

Привет, мужчины Омска! Для вас открывается новый мир увлекательного досуга с девушками благодаря новому сайту в вашем городе. Вас ждут множество анкет женщин, готовых провести с вами время. Погружайтесь в атмосферу общительности и наслаждайтесь приятными моментами – https://omsk-night.net/

account selling service https://social-accounts-marketplace.live

account buying service https://buy-accounts.live

account exchange service https://accounts-marketplace.online/

profitable account sales https://accounts-marketplace-best.pro

маркетплейс аккаунтов магазины аккаунтов

площадка для продажи аккаунтов https://rynok-akkauntov.top

маркетплейс аккаунтов kupit-akkaunt.xyz

маркетплейс аккаунтов соцсетей akkaunt-magazin.online

купить аккаунт akkaunty-market.live

магазин аккаунтов https://kupit-akkaunty-market.xyz/

Знакомства с более чем 1500 реальными девушками Краснодара ждут вас на нашем сайте, где каждый сможет открыть что-то новое https://krasnodar-indi.life/

купить аккаунт https://akkaunty-optom.live

маркетплейс аккаунтов соцсетей online-akkaunty-magazin.xyz

טיפולי, אף שמוכר בעיקר בזכות היתרונות הרפואיים שלו בקידום ריפוי גופני נהנים אותך. תאמיני לי, זו החוויה של פעם בחיים ואת לא רוצה לפספס.” go to link

продать аккаунт akkaunty-dlya-prodazhi.pro

שלה, השלימה את הביטחון השקט והשנינות החריפה של גיטה, ויצרה צמד דינמי ידעו שהם נכנסים לפרק חדש בחייהם, מלא באפשרויות ואתגרים. העיר השוקקת ליווי בירושלים

גמיש יותר. זמינות במגוון טעמים וצורות: פונה לקהל רחב יותר. חסרונות דבריה עשויה להצביע על כך שהיא תהיה בסדר אם “יאכזב את השמירה שלו”. נערת ליווי בקריות

маркетплейс аккаунтов соцсетей kupit-akkaunt.online

בשיחה שמגלה עניין וכבוד אמיתי כלפיה כאדם. זכרו, בניית קשר המבוסס על גם טרנספורמציה של זהותם ושאיפותיהם. כשהם משאירים מאחור את המוכר בננה סקס

לצרכים הספציפיים שלכם. בין אם אתם מחפשים עיסוי רקמות עמוק כדי להקל על מאחורי החזית הצנועה של דירה דיסקרטית בראשון לציון מסתתר עולם שמעטים browse this sitesays:

ליווי בגרמניה, שעובדת כדי לממן את הלימודים ולקנות מותרות. בדיוק כפי דירות דיסקרטיות בגבעתיים אנחנו יכולים ליהנות מהפרטיות של המרחב מבלי find out here

השאלון שלי והוא אמר לי שהוא סיפק שירותים דומים. מארק אמר שהוא היה המסורתי של נערות ליווי במרכז. גדלתי במשפחה שמעולם לא היה בה כסף בשפע, click this over here now

https://simpson.com.tr/konu/tamprost-kullanmaya-basladim-ama-bazi-degisiklikler-fark-ettim.4074/

חיי לקוחותיה. תחושת העצמה אישית זו מתדלקת את החתירה לחופש ומלבינה את לה, חייב לעשות את זה שוב. אחרי הכול מה לא עושים בשביל לטפח מערכת visit their website

fb account for sale https://buy-adsaccounts.work/

facebook ads accounts https://buy-ad-accounts.click

buy a facebook ad account https://buy-ad-account.top

תהליכים שנראו עד לא מזמן קשים. היא סיננה בדיוק את מי שצריך ולא לקח לה שלה שהיא עשתה את המעשה. נפגש עם סקרלט במקום מבודד בצורה מועילה. כנראה discover here

buy facebook accounts cheap https://buy-ads-account.click/

Побываете этот веб-сайт https://www.kamekin.co.jp/the-best-place-to-invest-your-money/

buy facebook old accounts fb account for sale

buy a facebook ad account buy facebook accounts for advertising

buy facebook ads accounts https://ad-account-for-sale.top

buy facebook profiles https://buy-ad-account.click

Эта статья предлагает уникальную подборку занимательных фактов и необычных историй, которые вы, возможно, не знали. Мы постараемся вдохновить ваше воображение и разнообразить ваш кругозор, погружая вас в мир, полный интересных открытий. Читайте и открывайте для себя новое!

Изучить вопрос глубже – https://medalkoblog.ru/

Приедете в текущий веб-сайт https://happyfishes.ru/product/315351/

buy fb ad account https://ad-accounts-for-sale.work

buy google adwords account https://buy-ads-account.top/

buy google ads threshold account https://buy-ads-accounts.click

buy fb ad account https://buy-accounts.click

order valacyclovir pills – order valacyclovir 1000mg without prescription purchase fluconazole pill

buy google ads invoice account https://ads-account-for-sale.top

buy verified google ads accounts buy adwords account

Навестите текущий сайт https://okusurijoho.com/2021/09/30/hello-world/

buy google ads account https://buy-ads-invoice-account.top

buy aged google ads accounts buy-account-ads.work

buy google ads agency account https://buy-ads-agency-account.top

google ads agency account buy https://sell-ads-account.click

Посетите текущий сайт https://www.usb-tec.com/portfolio/parallel-platforms/

buy verified google ads accounts https://ads-agency-account-buy.click

buy facebook business managers https://buy-business-manager.org/

Приедете в этот сайт https://shinpeak.com/how-many-organs-in-human-body/comment-page-548/

adwords account for sale https://buy-verified-ads-account.work/

Start your future with a Bachelor’s in Robotics and Automation at Satbayev University. Explore admission deadlines, required documents, and study options. Perfect for international students pursuing robotics, control systems, industrial automation – https://satbayev.university/

buy facebook ads accounts and business managers buy-bm-account.org

facebook bm for sale https://buy-business-manager-acc.org/

buy facebook bm https://buy-verified-business-manager-account.org

buy bm facebook https://buy-verified-business-manager.org

Приедете в этот веб-сайт https://www.srmotorbodies.co.uk/home-page/attachment/alloy-1/#main/

buy business manager https://business-manager-for-sale.org

business manager for sale buy-business-manager-verified.org

buy fb bm https://buy-bm.org

https://planet-today.ru/stati/health/item/181173-perelomy-osnovnye-vidy-simptomy-diagnostika-i-lechenie

buy verified business manager facebook https://verified-business-manager-for-sale.org/

Посетите текущий сайт http://pearlbd.com/development-of-digital-land-record/1-4/

buy verified business manager https://buy-business-manager-accounts.org

tiktok ads account for sale https://buy-tiktok-ads-account.org

tiktok ad accounts https://tiktok-ads-account-buy.org

раскрутка тг канала бесплатно живые подписчики

Актуальные новости. Все про политику, культуру, общество, спорт и многое другое ежедневно на страничках нашего популярного аналитического блога https://mozhga18.ru/

tiktok ads agency account https://tiktok-ads-account-for-sale.org

tiktok ad accounts https://tiktok-agency-account-for-sale.org

tiktok ads agency account https://buy-tiktok-ad-account.org

Актуальные статьи с полезными советами по строительству и ремонту. Каждый найдет у нас ответы на самые разнообразные вопросы по ремонту https://masteroff.org/

buy tiktok ads account https://buy-tiktok-ads-accounts.org

Releasing the fear of not being “enough” makes space for authenticity and healing with cheap generic viagra lowest prices. Order discreetly and let privacy be your strength.

Новости экономики России, зарплаты и кредиты, обзоры профессий, идеи бизнеса и истории бизнесменов. Независимая экономическая аналитика и репортажи https://iqreview.ru/

накрутка подписчиков в телеграм канал

https://www.asseenontvonline.ru/

Старый Лекарь болезни и лечение – Лекарь расскажет: лекарственные травы, болезни и лечение, еда, массаж, диеты и правильное питание https://old-lekar.com/

buy tiktok ad account https://buy-tiktok-business-account.org

tiktok ads account for sale https://buy-tiktok-ads.org

buy tiktok ads https://tiktok-ads-agency-account.org

Самые интересные и полезные статьи на тему настройки и оптимизации работы компьютеров и оргтехники https://www.softo-mir.ru/

Актуальные мировые события. Последние новости, собранные с разных уголков земного шара. Мы публикуем аналитические статьи о политике, экономике, культуре, спорте, обществе и многом ином https://informvest.ru/

Блог, посвященный любителям самоделок. Интересные статьи по теме стройки и ремонта, авто, сада и огорода, вкусных рецептов, дизайна и много другого, что каждый может сделать своими руками https://notperfect.ru/

Все для планшетов – новости, обзоры устройств, игр, приложений, правильный выбор, ответы на вопросы https://protabletpc.ru/

Ежедневные публикации про новинки автомобилей, советы по ремонту и эксплуатации, мастер-классы тюнинга, новое в правилах ПДД и автомобильных законах в нашем блоге https://mineavto.ru/

СамСтрой. Блог о ремонте и строительтве для каждого! Полезные советы, фото и видео материалы про стройку и ремонт, дизайн интерьера, а также приусадебный участок https://biosferapark.ru/

What’s up mates, its enormous piece of writing concerning teachingand completely explained, keep it up all the time.

aralash jang

Hi there to every , since I am genuinely keen of reading this web site’s post to be updated daily. It carries good information.

mel bet

Keep on working, great job!

bus card recharge near me

https://www.ukrinformer.com.ua/pogoda-v-bilij-cerkvi/

https://ukrainedigest.com.ua/pohoda-v-brovarakh/

Pretty! This has been a really wonderful article. Thanks for supplying these details.

https://postheaven.net/purplehome9/henry-uz-the-legacy-of-anri-barcelona-in-modern-sport

кайт школа хургада

An impressive share! I’ve just forwarded this onto a co-worker who had been doing a little research on this. And he in fact bought me breakfast because I discovered it for him… lol. So allow me to reword this…. Thank YOU for the meal!! But yeah, thanx for spending some time to talk about this topic here on your web site.

https://maps.google.nr/url?q=https://beckham-uz.com/

cialis 5 mg prezzo in farmacia con ricetta : an effective drug containing tadalafil, is used for erectile dysfunction and benign prostatic hyperplasia. In Italy, a 28-tablet pack of Cialis 5 mg costs around €165.26, though prices vary by pharmacy and discounts. Generic alternatives, like Tadalafil DOC Generici, range from €0.8–€2.6 per tablet, providing a budget-friendly choice. Consult a doctor, as a prescription is required.

кайт сафари

Very good blog you have here but I was wanting to know if you knew of any community forums that cover the same topics discussed in this article? I’d really love to be a part of online community where I can get opinions from other experienced individuals that share the same interest. If you have any suggestions, please let me know. Many thanks!

https://tehnoprice.in.ua/shokery-protiv-napadayushchikh-kak-zashchitit-sebya-v-opasnoy-situatsii

«Рентвил» предлагает аренду автомобилей в Краснодаре без залога и ограничений по пробегу по Краснодарскому краю и Адыгее. Требуется стаж от 3 лет и возраст от 23 лет. Оформление за 5 минут онлайн: нужны только фото паспорта и прав. Подача авто на жд вокзал и аэропорт Краснодар Мин-воды Сочи . Компания работает 10 лет , автомобили проходят своевременное ТО. Доступны детские кресла. Бронируйте через сайт Аренда авто в Краснодаре

https://www.wpdis.co/kak-vyibrat-narkologicheskuyu-kliniku-ischerpyivayushhee-rukovodstvo/

температура воды хургада

Can I simply just say what a comfort to uncover a person that truly understands what they are talking about online. You definitely know how to bring an issue to light and make it important. More and more people have to read this and understand this side of your story. It’s surprising you aren’t more popular because you surely possess the gift.

https://tayger.com.ua/vidguki-koristuvachiv-pro-linzi-v-fary-dosvid-ta-rekomendatsiyi

https://oboronspecsplav.ru/

Пассажирские перевозки Томск – Астана Развитая сеть пассажирских перевозок играет ключевую роль в обеспечении мобильности населения и укреплении экономических связей между регионами. Наша компания специализируется на организации регулярных и безопасных поездок между городами Сибири и Казахстана, предлагая комфортные условия и доступные цены.

«Рентвил» предлагает аренду автомобилей в Краснодаре без залога и ограничений по пробегу по Краснодарскому краю и Адыгее. Требуется стаж от 3 лет и возраст от 23 лет. Оформление за 5 минут онлайн: нужны только фото паспорта и прав. Подача авто на жд вокзал и аэропорт Краснодар Мин-воды Сочи . Компания работает 10 лет , автомобили проходят своевременное ТО. Доступны детские кресла. Бронируйте через сайт Прокат авто Краснодар

Токарные патроны Bison Токарные патроны Bison Запчасти для станков Bison Bial В мире металлообработки, где точность и надежность играют ключевую роль, токарные патроны Bison занимают особое место. Эти инструменты, производимые известной польской компанией Bison Bial, зарекомендовали себя как высококачественные и долговечные компоненты для токарных станков. Они обеспечивают надежный зажим заготовок, что напрямую влияет на качество и скорость обработки.

I’m not sure exactly why but this web site is loading extremely slow for me. Is anyone else having this problem or is it a issue on my end? I’ll check back later and see if the problem still exists.

Myzain

This is really interesting, You are a very skilled blogger. I’ve joined your rss feed and look forward to seeking more of your great post. Also, I’ve shared your web site in my social networks!

Zain recharge

Выкуп с 1688 В эпоху глобализации и стремительного развития мировой экономики, Китай занимает ключевую позицию в качестве крупнейшего производственного центра. Организация эффективных и надежных поставок товаров из Китая становится стратегически важной задачей для предприятий, стремящихся к оптимизации затрат и расширению ассортимента. Наша компания предлагает комплексные решения для вашего бизнеса, обеспечивая бесперебойные и выгодные поставки товаров напрямую из Китая.

Мебель для кухни Кухня – сердце дома, место, где рождаются кулинарные шедевры и собирается вся семья. Именно поэтому выбор мебели для кухни – задача ответственная и требующая особого подхода. Мебель на заказ в Краснодаре – это возможность создать уникальное пространство, идеально отвечающее вашим потребностям и предпочтениям.

В динамичном мире Санкт-Петербурга, где каждый день кипит жизнь и совершаются тысячи сделок, актуальная и удобная доска объявлений становится незаменимым инструментом как для частных лиц, так и для предпринимателей. Наша платформа – это ваш надежный партнер в поиске и предложении товаров и услуг в Северной столице. Свежие объявления

варфейс аккаунт В мире онлайн-шутеров Warface занимает особое место, привлекая миллионы игроков своей динамикой, разнообразием режимов и возможностью совершенствования персонажа. Однако, не каждый готов потратить месяцы на прокачку аккаунта, чтобы получить желаемое оружие и экипировку. В этом случае, покупка аккаунта Warface становится привлекательным решением, открывающим двери к новым возможностям и впечатлениям.

Remarkable! Its truly amazing article, I have got much clear idea concerning from this paragraph.

hafilat card

музыкальные новинки Роп – Русский роп – это больше, чем просто музыка. Это зеркало современной российской души, отражающее её надежды, страхи и мечты. В 2025 году жанр переживает новый виток развития, впитывая в себя элементы других стилей и направлений, становясь всё более разнообразным и эклектичным. Популярная музыка сейчас – это калейдоскоп звуков и образов. Хиты месяца мгновенно взлетают на вершины чартов, но так же быстро и забываются, уступая место новым музыкальным новинкам. 2025 год дарит нам множество талантливых российских исполнителей, каждый из которых вносит свой неповторимый вклад в развитие жанра.

modafinil 100mg tablet buy modafinil 200mg without prescription provigil buy online provigil 200mg for sale provigil online buy cheap modafinil 200mg provigil online

Сергей Бидус кидало

For most up-to-date news you have to go to see the web and on world-wide-web I found this web site as a best web site for newest updates.

kinai porno

Pretty section of content. I just stumbled upon your site and in accession capital to assert that I get in fact enjoyed account your blog posts. Anyway I will be subscribing to your augment and even I achievement you access consistently rapidly.

hafilat balance check

chicken road game apk Chicken Road: Взлеты и Падения на Пути к Успеху Chicken Road – это не просто развлечение, это обширный мир возможностей и тактики, где каждое решение может привести к невероятному взлету или полному краху. Игра, доступная как в сети, так и в виде приложения для мобильных устройств (Chicken Road apk), предлагает пользователям проверить свою фортуну и чутье на виртуальной “куриной тропе”. Суть Chicken Road заключается в преодолении сложного маршрута, полного ловушек и опасностей. С каждым успешно пройденным уровнем, награда растет, но и увеличивается шанс неудачи. Игроки могут загрузить Chicken Road game demo, чтобы оценить механику и особенности геймплея, прежде чем рисковать реальными деньгами.

roobet promo code WEB3 В мире онлайн-казино инновации не стоят на месте, и Roobet находится в авангарде этих перемен. С появлением технологии Web3, Roobet предлагает игрокам новый уровень прозрачности, безопасности и децентрализации. Чтобы воспользоваться всеми преимуществами этой передовой платформы, используйте промокод WEB3.

Крыша на балкон Балкон, прежде всего, – это открытое пространство, связующее звено между уютом квартиры и бескрайним внешним миром. Однако его беззащитность перед капризами погоды порой превращает это преимущество в существенный недостаток. Дождь, снег, палящее солнце – все это способно причинить немало хлопот, лишая возможности комфортно проводить время на балконе, а также нанося ущерб отделке и мебели. Именно здесь на помощь приходит крыша на балкон – надежная защита и гарантия комфорта в любое время года.

Rainbet redeem affiliate code ILBET Откройте для себя все преимущества Rainbet, используя промокод ILBET при регистрации или пополнении счета. Этот код активирует эксклюзивные бонусы, акции и специальные предложения, разработанные специально для вас, чтобы сделать ваше игровое приключение еще более прибыльным и увлекательным.

Навес – практичное решение для тех, кто хочет уберечь автомобиль от солнца, дождя, снега и других капризов погоды, не строя капитальный гараж. Он быстрее возводится, дешевле в установке и может быть адаптирован под любые нужды. В этой статье мы расскажем, какие бывают виды навесов, из каких материалов их делают, и как выбрать конструкцию, которая прослужит долго и гармонично впишется в участок: недорогие навесы для дачи

pinco bet Pinco, Pinco AZ, Pinco Casino, Pinco Kazino, Pinco Casino AZ, Pinco Casino Azerbaijan, Pinco Azerbaycan, Pinco Gazino Casino, Pinco Pinco Promo Code, Pinco Cazino, Pinco Bet, Pinco Yukl?, Pinco Az?rbaycan, Pinco Casino Giris, Pinco Yukle, Pinco Giris, Pinco APK, Pin Co, Pin Co Casino, Pin-Co Casino. Онлайн-платформа Pinco, включая варианты Pinco AZ, Pinco Casino и Pinco Kazino, предлагает азартные игры в Азербайджане, также известная как Pinco Azerbaycan и Pinco Gazino Casino. Pinco предоставляет промокоды, а также варианты, такие как Pinco Cazino и Pinco Bet. Пользователи могут загрузить приложение Pinco (Pinco Yukl?, Pinco Yukle) для доступа к Pinco Az?rbaycan и Pinco Casino Giris. Pinco Giris доступен через Pinco APK. Pin Co и Pin-Co Casino — это связанные термины.

Ментор Разработка стратегии: создайте уникальный путь к успеху. Без четкой стратегии ваш бизнес рискует потеряться в море конкурентов. Настоящий успех достигается через продуманную и гибкую стратегию, которая учитывает все риски и возможности. Ментор поможет вам определить сильные стороны, сформировать уникальное предложение и разработать план действий. Вместе вы создадите дорожную карту, которая приведет к росту и устойчивости. Не позволяйте неопределенности мешать развитию — инвестируйте в профессиональную поддержку и создайте рабочую стратегию. Закажите консультацию, начните путь к успеху.

температура воды в хургаде в апреле

совкомбанк дебетовая карта онлайн Ваш доверенный эксперт в мире банковских карт. Получение современной дебетовой карты стало простым и удобным с нашей помощью. Выберите карту, которая наилучшим образом соответствует вашим потребностям, и используйте все преимущества современного финансового сервиса. Что мы предлагаем? Полезные советы: Полезные лайфхаки и рекомендации для эффективного использования вашей карты. Актуальные акции: Будьте в курсе всех новых предложений и специальных условий от банков-партнеров. Преимущества нашего сообщества. Мы предоставляем полную информацию о различных типах карт, особенностях тарифов и комиссий. Наши публикации регулярно обновляются, предоставляя актуальные данные и свежие новости о продуктах российских банков. Присоединяйтесь к нашему сообществу, чтобы сделать ваши финансовые решения простыми, быстрыми и надежными. Вместе мы сможем оптимизировать использование банковских продуктов и сэкономить ваше время и средства. Наша цель — помогать вам эффективно управлять своими финансами и получать максимум выгоды от каждого взаимодействия с банком.

https://community.jmp.com/t5/user/viewprofilepage/user-id/62239 vidalista super active

работа моделью онлайн в Польше Стань вебкам моделью в польской студии, работающей в Варшаве! Открыты вакансии для девушек в Польше, особенно для тех, кто говорит по-русски. Ищешь способ заработать онлайн в Польше? Предлагаем подработку для девушек в Варшаве с возможностью работы в интернете, даже с проживанием. Рассматриваешь удаленную работу в Польше? Узнай, как стать вебкам моделью и сколько можно заработать. Работа для украинок в Варшаве и высокооплачиваемые возможности для девушек в Польше ждут тебя. Мы предлагаем легальную вебкам работу в Польше, онлайн работа без необходимости знания польского языка. Приглашаем девушек без опыта в Варшаве в нашу вебкам студию с обучением. Возможность заработка в интернете без вложений. Работа моделью онлайн в Польше — это шанс для тебя! Ищешь “praca dla dziewczyn online”, “praca webcam Polska”, “praca modelka online” или “zarabianie przez internet dla kobiet”? Наше “agencja webcam Warszawa” и “webcam studio Polska” предлагают “praca dla mlodych kobiet Warszawa” и “legalna praca online Polska”. Смотри “oferty pracy dla Ukrainek w Polsce” и “praca z domu dla dziewczyn”.

купить компьютер под заказ Игровые компьютеры на заказ: Индивидуальность и мощность Игровые компьютеры на заказ – это возможность создать уникальную машину, отражающую ваш стиль и предпочтения. Выберите корпус, систему охлаждения, подсветку и другие элементы, чтобы сделать ваш компьютер неповторимым.

кайтсёрфинг

кайт блага Кайт Анапа – это больше, чем просто увлечение, это образ жизни, вдохновленный солнцем, ветром и морской свежестью. Анапа, благодаря своим широким пляжам и устойчивым ветрам, превратилась в привлекательное место для поклонников кайтсерфинга. Здесь можно встретить как новичков, делающих первые шаги с опытными инструкторами, так и профессионалов, совершенствующих свое мастерство в захватывающих трюках. Кайт школа в Анапе – это кузница будущих звезд кайтсерфинга. Школы предлагают разнообразные программы обучения для всех уровней, от начальных курсов до продвинутых тренировок. Профессиональные инструкторы, качественное оборудование и индивидуальный подход гарантируют быстрый прогресс и безопасность на воде. Кайт школа в Анапе – это не только уроки, но и дружное сообщество, объединенное страстью к ветру и морю. Здесь легко найти друзей, получить советы и приятно провести время в кругу единомышленников. Кайтсерфинг в Анапе – это шанс отвлечься от повседневности, ощутить свободу и испытать незабываемые эмоции. Представьте себя, скользящим по волнам, подгоняемым ветром, в окружении чаек и под ласковым солнцем. Это не просто спорт, это приключение, которое останется в памяти навсегда. Кайтсерфинг в Благовещенской – еще одно популярное место в Анапском районе. Здесь, на просторной косе между Бугазским лиманом и Черным морем, созданы идеальные условия для катания. Мелководье и стабильный ветер делают Благовещенскую отличным местом для обучения. Кайт Блага – это сокращенное название Благовещенской, используемое кайтсерферами. Здесь есть несколько кайт-станций, предлагающих обучение, прокат и хранение оборудования. Кайтсерфинг в Анапе – это выбор тех, кто ценит активный отдых, любит ветер и море и готов к новым вызовам. Присоединяйтесь к сообществу и откройте для себя мир захватывающих приключений! DETIVETRA (ДЕТИ ВЕТРА) – это не просто название, это жизненная философия. Это те, кто чувствует ветер, не боится перемен и всегда готов к новым открытиям. Присоединяйтесь к ДЕТЯМ ВЕТРА и ощутите себя частью чего-то большего!

This is my first time visit at here and i am really impressed to read all at one place.

abu dhabi bus card where to buy

With thanks. Loads of erudition!

Psychological barriers to sex are easier to overcome when supported by consistent use of buy viagra pfizer online. Reclaiming your strength doesn’t erase the journey – it honors every step you took to get back up.

More posts like this would make the blogosphere more useful.

zithromax generic – metronidazole for sale oral metronidazole

Vidalista obat apa: vidalista.homes – Vidalista 500 mg l-arginina

buy semaglutide generic – periactin canada cheap periactin 4 mg

domperidone 10mg us – order generic flexeril buy generic flexeril

inderal order online – methotrexate 5mg us order methotrexate 10mg for sale

отдых на море цены на 2025 Кайт центр — это место, где можно арендовать оборудование и получить консультации от опытных инструкторов. Центры расположены на лучших пляжах, что обеспечивает удобный доступ к воде и ветру.

dapoxetine generic: duralast 30 – priligy 90 mg

amoxicillin over the counter – buy amoxil paypal order combivent 100 mcg online

Useful information. Fortunate me I found your site accidentally, and I’m shocked why this accident did not took place in advance! I bookmarked it.

tadalafil doc 5 mg 28 compresse prezzo

Wow, superb blog layout! How long have you been blogging for? you made blogging look easy. The overall look of your web site is great, as well as the content!

Dismemberment

шторы тюль Купить рулонные шторы – это значит сделать выбор в пользу практичности и функциональности. Штора без

авто в аренду в Краснодаре аренда автомобилей краснодар: Большой автопарк, доступные цены и высокий уровень сервиса – все, что нужно для вашего комфортного путешествия.

Как сделать потолок В Реутове натяжные потолки – это оптимальное решение для тех, кто ищет сочетание цены и качества. Окна ПВХ Малаховка

1000 рублей за регистрацию вывод сразу 1000 рублей без депозита

I loved as much as you’ll receive carried out right here. The sketch is attractive, your authored subject matter stylish. nonetheless, you command get bought an impatience over that you wish be delivering the following. unwell unquestionably come more formerly again as exactly the same nearly very often inside case you shield this hike.

tadalafil lilly 5 mg prezzo

buy azithromycin 250mg for sale – tindamax 500mg price order nebivolol 20mg online cheap

игровые автоматы бонус 1000 рублей за регистрацию без депозита Бездепозитный бонус в размере 1000 рублей с моментальным выводом – это редкая и ценная находка для азартных игроков. Она позволяет начать игру, не вкладывая собственные средства, и сразу же вывести выигрыш, если повезет. 1000 рублей за регистрацию вывод сразу без вложений

Why visitors still make use of to read news papers when in this technological world everything is accessible on net?

cialis 5 mg cialis prezzo

best cargo company in uae China to Dubai: Financing Options for International Trade

пионы москва Заказать пионы в Москве: Удобство и простота в каждом клике. Наш онлайн-сервис разработан с учетом потребностей самых занятых людей. Заказать пионы в Москве стало проще простого: выберите понравившийся букет на нашем сайте, укажите адрес доставки и удобное время, и мы позаботимся обо всем остальном. Мы гарантируем не только безупречное качество цветов, но и быструю и надежную доставку.

скачать игры без торрента Скачать игры с облака Mail: Играйте где угодно, когда угодно. Облако Mail – это ваша мобильная библиотека игр, всегда под рукой. Загружайте, скачивайте и запускайте игры на любом устройстве, имеющем доступ к интернету. Насладитесь свободой и гибкостью, выбирая из постоянно пополняющегося каталога.

buy generic augmentin online – https://atbioinfo.com/ buy cheap generic acillin

Бездепозитные бонусы Прежде чем принять щедрое предложение от казино, стоит внимательно изучить условия предоставления бездепозитного бонуса. Важно обратить внимание на вейджер – коэффициент, который определяет, сколько раз нужно отыграть бонус, прежде чем вывести выигрыш. Также стоит обратить внимание на сроки действия бонуса и ограничения по играм. Тщательное изучение правил поможет избежать разочарований и максимально эффективно использовать бонус для достижения своих целей.

Когда я зашёл на эту платформу, ощущение было таким, будто я отправился в путешествие. Здесь каждая ставка — это не просто волнение, а история, которую ты ощущаешь с каждым вращением.

Дизайн создан для комфорта, словно легкое прикосновение направляет тебя от момента к моменту. Транзакции, будь то депозиты или вывод средств, проходят плавно, как поток воды, и это удивляет. А техподдержка всегда готова подхватить, как друг, который никогда не подведёт.

Для меня Селектор онлайн стал миром, где азарт и искусство сплетаются. Здесь каждый момент — это часть истории, которую хочется переживать снова и снова.

кайтсёрфинг Хуркаде плавают акулы: ситуация с акулами Хуркаде плавают акулы: ситуация контролируется.

кто ремонтирует посудомойки на дому алматы Мастер по ремонту посудомоечных машин Алматы: Вызов мастера на дом.

generic esomeprazole 40mg – https://anexamate.com/ buy nexium generic

купить фольксваген Автомобили бу: Как выбрать достойный вариант При выборе автомобиля бу важно обратиться к проверенным продавцам и тщательно проверить его историю.

https://2-bs2best.lat/bs2_best_at.html

Phenylnitropropene Ephedrine is often used to produce phenylacetone, a key intermediate in stimulant synthesis. From phenylacetone, substances like methylone, mephedrone (4-MMC), and 3-CMC can be made using methylamine. Phenylnitropropene, derived from nitroethane, is another precursor. A-PVP and 4-methylpropiophenone are also widely used in synthetic drug production. BMK glycidate is commonly used to synthesize controlled substances.

Благоустройство территории

coumadin for sale – cou mamide cozaar 25mg drug

https://2-bs2best.art/index.html

4-methylpropiophenone Ephedrine is often used to produce phenylacetone, a key intermediate in stimulant synthesis. From phenylacetone, substances like methylone, mephedrone (4-MMC), and 3-CMC can be made using methylamine. Phenylnitropropene, derived from nitroethane, is another precursor. A-PVP and 4-methylpropiophenone are also widely used in synthetic drug production. BMK glycidate is commonly used to synthesize controlled substances.

https://2-bs2best.art/blaksprut_ssylka.html

https://1-bs2best.lat/blacksprut_zerkalo.html

вавада казино официальный сайт вход бесплатный играть Вавада казино открывает двери в мир азарта и возможностей, предлагая пользователям прямой доступ к обширной коллекции игр и захватывающим бонусам. Официальный сайт – это надежная платформа, где каждый игрок может насладиться честной игрой и безопасными транзакциями. Легкость навигации и интуитивно понятный интерфейс делают вход и начало игры максимально простыми и удобными. Vavada Casino Скачать

https://2-bs2best.lat/blacksprut_bs2best.html

Aw, this was an incredibly good post. Taking the time and actual effort to produce a great article… but what can I say… I procrastinate a whole lot and never manage to get nearly anything done.

https://jiraf.com.ua/linza-v-avtofari-iak-vybraty

Are you looking for new ways to enrich your spiritual journey or simply want to try out some interesting mystical practices? I found a great article that covers a variety of magical rituals and traditions worth exploring. Whether you’re a beginner or already familiar with spiritual practices, you’ll find something valuable here: magic rituals. It’s a great starting point for anyone interested in the world of divination and self-discovery.

https://2-bs2best.art/https_bs2best_at.html

buy meloxicam 7.5mg sale – moboxsin.com meloxicam without prescription

1000 рублей за регистрацию в казино без депозита Получить 1000 рублей за регистрацию с моментальным выводом, не требующим каких-либо вложений, – это мечта любого новичка онлайн-казино. Это возможность начать игру с преимуществом и испытать свою удачу без финансового риска.

online nyerogep

https://2-bs2best.art/bs2best_at.html

https://a-bsme.at/bs2best_at.html

Бездепозитные бонусы Бездепозитные бонусы

психиатрическая клиника Психиатрическая клиника. Само это словосочетание вызывает в воображении образы, окутанные туманом страха и предрассудков. Белые стены, длинные коридоры, приглушенный свет – все это лишь проекции нашего собственного внутреннего смятения, отражение боязни заглянуть в темные уголки сознания. Но за этими образами скрывается мир, полный боли, надежды и, порой, неожиданной красоты. В этих стенах встречаются люди, чьи мысли и чувства не укладываются в рамки общепринятой “нормальности”. Они борются со своими демонами, с голосами в голове, с навязчивыми идеями, которые отравляют их существование. Каждый из них – это уникальная история, сложный лабиринт переживаний и травм, приведших к этой точке. Здесь работают люди, посвятившие себя помощи тем, кто оказался на краю. Врачи, медсестры, психологи – они, как маяки, светят в ночи, помогая найти путь к выздоровлению. Они не волшебники, и не всегда могут исцелить, но их сочувствие, их понимание и профессионализм – это часто единственная нить, удерживающая пациента от окончательного падения в бездну. Жизнь в психиатрической клинике – это не заточение, а скорее передышка. Время для того, чтобы собраться с силами, чтобы разобраться в себе, чтобы научиться жить со своими особенностями. Это место, где можно найти поддержку, где можно не бояться быть собой, даже если этот “себя” далек от идеала. И хотя выход из клиники не гарантирует безоблачного будущего, он дает шанс на новую жизнь, на жизнь, в которой найдется место для радости, для любви и для надежды.

https://b2tsite3.cc/blacksprut_bs2best.html

deltasone 5mg cheap – aprep lson cost deltasone 5mg

Подшипник цена Завод изготовитель подшипников – это предприятие с полным циклом производства, от разработки конструкторской документации до выпуска готовой продукции. Важно, чтобы завод имел необходимые сертификаты и соответствовал международным стандартам.

штора для ванной Шторы ночь — плотные ткани, которые полностью блокируют свет и создают комфортные условия для сна. Они часто используются в спальнях и детских комнатах, обеспечивая защиту от уличного освещения и создавая спокойную атмосферу для отдыха.

дворцы петербурга экскурсии Афиша Санкт-Петербург: Театры, концерты, выставки и другие мероприятия в Северной столице

Спортивные ставки Футбол ставки – самый популярный вид ставок. Большое количество лиг и матчей предоставляет широкий выбор для прогнозов.

Ventolin hfa 100 mcg inhaler price: albuterol hfa inhaler – Ventolin tabletten

where can i buy ed pills – male erection pills buy ed pills cheap

гибкая керамика для фасада дома Гибкая керамика для внутренней отделки монтаж не требует специальных клеевых составов, что упрощает процесс и снижает стоимость ремонта.

разработка позиционирования Частный маркетолог Анастасия Речанская предлагает индивидуальный подход к каждому клиенту, разрабатывая персонализированные стратегии, учитывающие специфику бизнеса и бюджет.

логистика led экранов IT инфраструктура школы под ключ IT инфраструктура школы под ключ от ТОО «Astana IT Garant» — это комплексное решение для создания современной цифровой среды образовательного учреждения. Мы проектируем и внедряем надежную, масштабируемую и безопасную IT-инфраструктуру, которая обеспечивает все потребности современной школы в информационных технологиях. Наша IT-инфраструктура включает серверное оборудование, системы хранения данных, сетевое оборудование, беспроводные точки доступа, системы безопасности и резервного копирования. Мы создаем отказоустойчивую архитектуру, обеспечивающую бесперебойную работу всех систем школы. Сетевая инфраструктура проектируется с учетом современных требований к пропускной способности и качеству обслуживания. Высокоскоростные каналы связи, управляемые коммутаторы, контроллеры беспроводных сетей обеспечивают стабильное подключение тысяч устройств одновременно. Astana IT Garant внедряет системы управления сетью, мониторинга производительности, контроля доступа и защиты от киберугроз. Централизованное управление всей IT-инфраструктурой упрощает администрирование и снижает эксплуатационные расходы. Облачные сервисы и виртуализация серверов повышают эффективность использования ресурсов и обеспечивают гибкость масштабирования. Системы автоматического резервного копирования защищают критически важные данные школы от потери, а планы восстановления после сбоев гарантируют быстрое возобновление работы.

игровой компьютер на заказ Собрать компьютер онлайн – это увлекательный процесс, позволяющий вам почувствовать себя инженером и создать уникальную систему.

amoxil usa – combamoxi.com purchase amoxil pill

The thoroughness in this break down is noteworthy.

Целительница Отзывы о целителях – важный источник информации при выборе специалиста. Важно обращать внимание на реальные отзывы и рекомендации других людей.

металлообработка Металлообработка – это обширная сфера деятельности, охватывающая широкий спектр процессов, направленных на изменение формы, размеров и свойств металлов и сплавов. От простых ручных операций до высокотехнологичных автоматизированных производств, металлообработка играет ключевую роль во многих отраслях промышленности, обеспечивая создание деталей, инструментов и конструкций, необходимых для функционирования современного мира.

spoofer hwid Где скачать Free HWID Spoofer: Безопасные источники

Aw, this was an exceptionally good post. Taking the time and actual effort to make a superb article… but what can I say… I hesitate a lot and don’t seem to get nearly anything done.

http://jamesrosenbarger.com/sklo-fary-pid-farbuvannya-koly-tse-dorechno.html

Онлайн казино России Маркетинг онлайн казино России: Стратегии и методы

cours d’acting a Paris Classes de theatre

работа военным Работа военным сопряжена с риском и опасностью, но она также дает возможность проявить себя, реализовать свой потенциал и внести свой вклад в защиту мира и стабильности.

https://stroidom36.ru/bystrovozvodimye-doma/ Кровля – защита от непогоды. Металлочерепица, профнастил, мягкая кровля – каждый материал имеет свои особенности в плане стоимости, долговечности и внешнего вида. Важно учитывать угол наклона крыши и климатические условия региона.

whoah this blog is wonderful i love reading your articles. Keep up the good work! You understand, many persons are looking around for this info, you can help them greatly.

https://mmartfashion.com/chy-mozhna-vstanovyty-sklo-fary-samomu-za-1-h.html

психология будущего Как справиться со стрессом: Эффективные техники и стратегии для управления стрессом и улучшения качества жизни.

This is a topic which is near to my verve… Numberless thanks! Quite where can I lay one’s hands on the acquaintance details in the course of questions?

Грузоперевозки Луганск Грузоперевозки газель Луганск: Перевозка грузов на автомобилях газель.

Очищение от негатива Как выйти из депрессии самостоятельно

Эфирные масла для духовного роста и самосовершенствования Эфирные масла doTERRA для здоровья. Натуральные помощники в укреплении иммунитета, облегчении дыхания, снятии мышечного напряжения. Лаванда для спокойствия, лимон для энергии, чайное дерево для защиты.

Грузоперевозки Луганск Перевозка негабаритных грузов Луганск: Организация перевозки негабаритных и тяжеловесных грузов.

More content pieces like this would urge the интернет better.

What’s up to all, how is all, I think every one is getting more from this site, and your views are fastidious in support of new users.

Cheap limo near me

завьялов илья поинт пей Илья Завьялов: Визионер, трансформирующий PointPay в глобальный финтех-гигант

купить макрос варфейс Затрудняетесь с установкой макроса? Узнайте, как установить макрос на варфейс правильно! Следуйте инструкциям, и вы сможете наслаждаться улучшенной стрельбой и контролем отдачи. Удачи!

завьялов илья поинт пей Илья Завьялов о Будущем Криптовалют и Point Pay

order fluconazole 200mg online – https://gpdifluca.com/# purchase fluconazole for sale

военная служба по контракту Контрактная служба: возможность получить образование, повысить квалификацию, стать профессионалом своего дела

Служба по контракту Служба по контракту: Путь к профессиональному мастерству и защите Отечества

мистическое читать Русские мистические истории – это рассказы о призраках, духах и других сверхъестественных существах, обитающих на территории России. Они отражают особенности русской культуры и мировоззрения, заставляя нас по-новому взглянуть на знакомые места.

Tor Network Bazaar Drugs Marketplace: A New Darknet Platform with Dual Access Bazaar Drugs Marketplace is a new darknet marketplace rapidly gaining popularity among users interested in purchasing pharmaceuticals. Trading is conducted via the Tor Network, ensuring a high level of privacy and data protection. However, what sets this platform apart is its dual access: it is available both through an onion domain and a standard clearnet website, making it more convenient and visible compared to competitors. The marketplace offers a wide range of pharmaceuticals, including amphetamines, ketamine, cannabis, as well as prescription drugs such as alprazolam and diazepam. This variety appeals to both beginners and experienced buyers. All transactions on the platform are carried out using cryptocurrency payments, ensuring anonymity and security. In summary, Bazaar represents a modern darknet marketplace that combines convenience, a broad product selection, and a high level of privacy, making it a notable player in the darknet economy.

Baixe imagens incríveis do fortune tiger png para sua diversão!

Участвуй в турнирах, активируй коды и начинай выигрывать прямо сейчас. [url=https://robbierist.com/]vavada bt7com[/url]

cenforce 100mg usa – order cenforce 50mg order generic cenforce 50mg

кайт хургада Кайтсерфинг и делегирование: Распределение задач

тепловизионное обследование Аренда строительных инструментов и оборудования за 5 минут и без залога! – оперативное обеспечение необходимым оборудованием.

buying facebook ad account account trading service account purchase

https://hyprcommunity.com/groups/vardenafil/ Levitra 20mg

где можно продать мед препараты в спб Ответственность за незаконную продажу Незаконная продажа лекарств влечет за собой административную или уголовную ответственность в зависимости от масштаба деятельности и нанесенного ущерба.

аренда инструментов Широкий ассортимент оборудования для любых строительных и ремонтных работ.

online cialis prescription – cialis shipped from usa cialis online canada ripoff

Химчистка мебели ростов Химчистка кожаной мебели в Ростове – деликатный уход за кожаными изделиями.

накрутка пф яндекс Накрутка ПФ: баланс между риском и выгодой Накрутка ПФ – это инструмент, требующий осторожного и взвешенного подхода. Вместо того, чтобы полагаться на сомнительные методы, лучше сосредоточиться на создании качественного и полезного сайта, который будет интересен реальным пользователям. Это – самый надежный путь к успеху в поисковой выдаче Яндекса.

facebook ad account buy account store account selling service

служба по контракту оренбург Преимущества службы по контракту в Оренбургской области: Служба по контракту в Оренбургской области предоставляет ряд преимуществ, включая стабильную заработную плату, возможность карьерного роста, обеспечение жильем и медицинским обслуживанием, а также возможность получения образования.

накрутка пф яндекс Риски накрутки ПФ: стоит ли играть с огнем? Использование “черных” методов накрутки ПФ может привести к серьезным последствиям, вплоть до исключения сайта из поисковой выдачи. Яндекс активно борется с искусственной активностью и применяет жесткие санкции к нарушителям.

сушенные лакомства Хрустящие субпродукты для чистки зубов: Здоровая улыбка вашего питомца Хрустящие сушеные субпродукты – это эффективное и безопасное средство для чистки зубов собаки. Они помогают удалить налет и зубной камень, предотвратить развитие заболеваний десен и сохранить здоровье полости рта вашего питомца.

Отличный обзор: от генератора чисел до стратегии ставок.: https://malimar.ru/wp-content/news/preimushestva_vavada_casino.html

tadalafil review forum – https://strongtadafl.com/ cialis 5mg daily how long before it works

ranitidine 150mg pill – ranitidine 150mg canada purchase ranitidine sale

Слив платных прогнозов бесплатно Диверсификация ставок: Снижение рисков Диверсификация ставок – это стратегия, которая позволяет снизить риски путем распределения ставок на разные события и исходы.

Фермы для ангара Каркас металлический для гаража Металлический каркас для гаража – это прочная и надежная основа для строительства гаража своими руками. Простота монтажа и долговечность конструкции делают его отличным выбором.

https://v-tagile.ru/obschestvo-iyul-5/kak-vybrat-idealnyj-buket-dlya-zhenshchiny-ot-povoda-do-yazyka-tsvetov

rexex Поменять криптовалюту Сделки по рынку помогут заработать.

More posts like this would make the internet a better place.

https://cleaninghouse24.ru

Драгон мани Стратегии Dragon money варьируются от агрессивных захватов до мирного развития. Важно учитывать экономические факторы, политические отношения и военную мощь. Умение адаптироваться к меняющимся условиям и принимать быстрые решения – ключ к победе.

https://altaywater.ru

Столица ночью не спит, и мы вдобавок: эксклюзивная центр лечения алкоголизма клиника mcnl.ru открыта 24/7. Без предварительной регистрации и документов — вызов доктора на дом за 39 минут, мягкий детокс под контролем, экспресс- капельница, психотерапия у вас, бессрочное сопровождение. Тайно, конфиденциально, точно — вернем вам трезвость без страха.

Игроки часто ищут вавада, и не зря — именно такие платформы обеспечивают честную игру и качественный сервис. Если вас интересует вавада, рекомендуем заглянуть сюда: вавада. Вы узнаете о бонусах, мобильной версии, рабочих зеркалах и многом другом. Проверяйте сами — вавада может приятно удивить!

лечебное голодание Голодание может быть эффективным инструментом для улучшения здоровья, но только при правильном подходе и под контролем специалистов.

Подшипники оптом от производителей Изготовитель подшипников – предприятие, специализирующееся на производстве и разработке подшипников различного типа и размера. Важно выбирать изготовителей с хорошей репутацией и опытом работы.

https://vdom-teplo.ru

Cамоустанавливающийся подшипник Шариковый подшипник Шариковые подшипники – универсальное решение для различных применений.

Thanks for sharing. It’s top quality. gabapentin 100mg without prescription

moneyport Платежный агент онлайн – это компания, которая предоставляет услуги платежного агента через интернет.

Hi, its pleasant article concerning media print, we all be familiar with media is a great source of data.

Luxury limo near me

Solpot Casino ensures secure, fair gaming Discover premium casino gaming now at solpot.xl-gamers.com https://solpot.xl-gamers.com Solpot Casino prioritizes responsible, secure play: Keep your data safe and game responsibly with Solpot Casino’s high standards!

This is the kind of writing I positively appreciate. https://ursxdol.com/sildenafil-50-mg-in/

bearing manufacturer in Europe where can i buy ball bearings: Uncover a dependable source for premium-quality ball bearings at competitive prices. Our extensive network of distributors and our user-friendly online platform offer convenient access to a vast selection of bearings from reputable manufacturers. Benefit from expert guidance, detailed product information, and seamless ordering to meet your specific requirements efficiently.

Hello are using WordPress for your site platform? I’m new to the blog world but I’m trying to get started and create my own. Do you require any coding knowledge to make your own blog? Any help would be really appreciated!

https://sytayaderevnya.ru/udalennoe-vedenie-biznesa-i-virtualnyj-nomer-v-kazahstane/

bearing manufacturer in Latvia buy ball bearings: Simplify your procurement journey with our comprehensive online platform, designed for seamless navigation and efficient ordering. We offer an expansive inventory of ball bearings sourced from leading manufacturers globally. Benefit from competitive pricing, detailed technical specifications, and secure transaction processing. Optimize your supply chain and ensure consistent quality by selecting from our curated collection of high-performance bearings.

реклама на вайлдберрис работа с карточками товара: Поддержка и оптимизация существующих карточек.

This is the compassionate of scribble literary works I truly appreciate. https://prohnrg.com/product/priligy-dapoxetine-pills/

стенд для выставки Изготовление стендов в Москве: Комплексный подход и индивидуальные решения Изготовление стендов в Москве – это комплексный подход, включающий в себя разработку концепции, дизайн, изготовление конструкций, монтаж и оформление. Важно выбрать компанию, которая предлагает индивидуальные решения, учитывающие все ваши пожелания и требования.

изготовление выставочных стендов москва Выставочный стенд заказать: Простота и удобство онлайн-сервисов Выставочный стенд заказать сегодня можно легко и быстро благодаря онлайн-сервисам. Многие компании предлагают возможность заказать стенд онлайн, выбрав из готовых шаблонов или предоставив индивидуальный дизайн-проект. Это позволяет сэкономить время и упростить процесс заказа.

Such a valuable bit of content.

Crash oyunlarının strategiyaları haqqında çox oxumuşdum, indi pincoazerbaijan.com/kazino-crash-oyunlari platformasında praktika edirəm və nəticələr yaxşıdır

amecapitals.com Отзывы Очень доволен результатами сотрудничества с AME Capitals.

Москва ночью бодрствует, а наша команда тоже всегда на страже: эксклюзивная наркологическая клиника https://mcnl.ru/ ждёт 24/7. Без записей и формальностей — выезд нарколога на дом, безопасный детокс в сне, ультрабыстрая капельница, психотерапия на дому, долговечное сопровождение. Без шума, анонимно, точно — вернем трезвость без боли.

https://frasesmotivacional.com/

http://xn--80aafabrjladsicc1amg1o4cf1dg.tech/

I particularly liked the way this was laid out.

кайтсёрфинг Кайтсёрфинг развивается очень быстро, появляются новые трюки, стили и оборудование. Это делает спорт еще более интересным и захватывающим.

More blogs like this would make the blogosphere more useful.

Fildena extra power: hitabs.com/fildena – Fildena 100mg

This is the kind of topic I enjoy reading. cialis et levitra

кайт школа “Сноукайтинг”: Кайтинг на лыжах или сноуборде

http://xn--80aafabrjladsicc1amg1o4cf1dg.press/

Such a practical insight.

купить офисную мебель от производителя “Атмосфера успеха”: мебель для кабинета руководителя – отражение статуса и корпоративной культуры, создание рабочей обстановки, сочетание функциональности и эстетики, важные элементы обстановки.

http://xn--80aafabrjladsicc1amg1o4cf1dg.online/

I took away a great deal from this.

доставка товаров из Китая Доставка сборного груза из Китая в Россию – это экономически выгодный способ транспортировки небольших партий товаров. Этот метод предполагает объединение нескольких небольших грузов в один контейнер, что позволяет снизить затраты на логистику. Важно тщательно упаковать груз и указать точную маркировку для избежания потери или путаницы.

Hi there, I desire to subscribe for this webpage to take newest updates, thus where can i do it please assist.

Local limo company near me

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

Купить тепловизор с доставкой по России (+ ЛНР, ДНР) Модульные одеяла из СВМПЭ: легкий и прочный щит от дронов. Доставка по России.

Стеклянные перегородки Стеклянные ограждения: правила безопасности и соответствие строительным нормам. Требования, сертификация и контроль качества.

где купить тепловизор аллмультикам тактическое снаряжение и экипировка Аллмультикам – популярная расцветка тактического снаряжения и экипировки.

https://servicestat.ru/service-spb Servicestat.ru — это удобный каталог-рейтинг сервисных центров по ремонту электроники. На сайте собраны контакты (адреса, телефоны), отзывы клиентов, акции и скидки, а также оценки качества услуг. Пользователи могут быстро найти проверенные мастерские в своем городе, сравнить рейтинги и выбрать лучший вариант. Полезен для тех, кто хочет отдать технику в надежные руки.

? Поиск сервисов по местоположению и брендам

? Реальные отзывы и оценки клиентов

? Акции, скидки и спецпредложения

? Удобный фильтр для сравнения услуг

Идеальный помощник в поиске надежного ремонта!

The breadth in this piece is exceptional.

хозблоки Утепление бытовки: как сделать бытовку пригодной для круглогодичного использования. Материалы для утепления, технологии утепления.

кайт Кайтсёрфинг – это комьюнити, где люди разных возрастов и профессий объединены общей страстью к приключениям и адреналину. Найдите своих единомышленников, путешествуйте вместе и делитесь опытом.

I found new insight from this.

кайтсёрфинг Кайтсёрфинг – это постоянное развитие и самосовершенствование. Учите новые трюки, осваивайте новые стили и делитесь опытом с другими кайтерами.

Such a helpful insight.

Since the admin of this site is working, no doubt very soon it will be renowned, due to its feature contents.

https://maps.google.mu/url?sa=t&url=https://cabseattle.com/

Драгон Мани Dragon Money – это не просто название, это врата в мир безграничных возможностей и захватывающих азартных приключений. Это не просто платформа, это целая вселенная, где переплетаются традиции вековых казино и новейшие цифровые технологии, создавая уникальный опыт для каждого искателя удачи. В современном мире, где финансовые потоки мчатся со скоростью света, Dragon Money предлагает глоток свежего воздуха – пространство, где правила просты, а возможности безграничны. Здесь каждая ставка – это шанс, каждый спин – это предвкушение победы, а каждый выигрыш – это подтверждение вашей удачи. Но Dragon Money – это не только про выигрыши и джекпоты. Это про сообщество единомышленников, объединенных общим стремлением к риску, азарту и адреналину. Это место, где можно найти новых друзей, поделиться опытом и ощутить неповторимый дух товарищества. Мы твердо верим, что безопасность и честность – это фундамент, на котором строится доверие. Именно поэтому Dragon Money уделяет особое внимание защите данных и обеспечению прозрачности каждой транзакции. Мы стремимся создать максимально комфортную и безопасную среду для наших игроков, где каждый может наслаждаться игрой, не беспокоясь о каких-либо рисках. Dragon Money – это не просто игра. Это возможность испытать себя, проверить свою удачу и почувствовать себя настоящим властелином своей судьбы. Присоединяйтесь к нам, и пусть дракон принесет вам богатство, успех и процветание! Да пребудет с вами удача!

https://familylab-spa.ru/

кайтинг “Страховка – твой ангел”: Как правильно использовать страховку и избежать травм

Thanks for sharing. It’s a solid effort.

Thanks for any other wonderful post. The place else could anyone get that type of information in such a perfect means of writing? I have a presentation next week, and I am on the look for such info.

https://images.google.cat/url?sa=t&url=https://seattlelimorates.com/

обучение кайтсёрфингу Кайтсёрфинг

More posts like this would make the online space better.

кайт лагерь Сноукайтинг: кайтинг на лыжах или сноуборде – техника и безопасность

кайтинг Кайтинг

I discovered useful points from this.

This is my first time pay a quick visit at here and i am actually pleassant to read everthing at alone place.

http://seabreeze.org.ua/5-rechej-yaki-ya-nikoly-ne-zroblyu-zi-sklom-f.html

кайтинг Кайтинг: стиль жизни, полный драйва. Откройте для себя мир кайтинга, сообщество увлеченных людей и новые горизонты.

This submission is outstanding.

This is my first time go to see at here and i am truly happy to read all at alone place.

how can i get cheap vermox no prescription

I absolutely liked the approach this was presented.

Today, I went to the beach with my children. I found a sea shell and gave it to my 4 year old daughter and said “You can hear the ocean if you put this to your ear.” She placed the shell to her ear and screamed. There was a hermit crab inside and it pinched her ear. She never wants to go back! LoL I know this is completely off topic but I had to tell someone!

buy doxycycline pill

micialisno.net: female cialis review – micialisno.net

you are actually a just right webmaster. The website loading pace is incredible. It kind of feels that you’re doing any distinctive trick. Also, The contents are masterwork. you’ve performed a great task on this subject!

https://maps.google.bg/url?sa=i&source=web&rct=j&url=https://seattlelimorates.com/

Such a informative bit of content.

IverCare Pharmacy: IverCare Pharmacy – IverCare Pharmacy

Greetings! Jolly productive recommendation within this article! It’s the petty changes which choice espy the largest changes. Thanks a lot quest of sharing! https://ondactone.com/spironolactone/

This article is excellent.

More articles like this would make the online space a better place.

Such a helpful insight.

AsthmaFree Pharmacy: AsthmaFree Pharmacy – AsthmaFree Pharmacy

Hi mates, its fantastic post concerning cultureand entirely defined, keep it up all the time.

Prezzi bassi farmaci online

compare ventolin prices: AsthmaFree Pharmacy – buy ventolin online australia

Thanks towards putting this up. It’s understandably done.

https://doxycyclinege.com/pro/meloxicam/

Situs judi resmi berlisensi: Link alternatif Beta138 – Bandar bola resmi

Jiliko bonus Jiliko slots Jiliko login

Mandiribet login: Situs judi resmi berlisensi – Slot jackpot terbesar Indonesia

Live casino Mandiribet: Mandiribet login – Slot gacor hari ini

https://jilwin.pro/# Jiliko casino walang deposit bonus para sa Pinoy

Online betting Philippines: Jollibet online sabong – jollibet

Swerte99 app: Swerte99 online gaming Pilipinas – Swerte99 login

Slot game d?i thu?ng Link vao GK88 m?i nh?t Rut ti?n nhanh GK88

Abutogel login: Abutogel – Link alternatif Abutogel

Bandar togel resmi Indonesia: Abutogel login – Jackpot togel hari ini

Abutogel: Abutogel – Jackpot togel hari ini

Beta138 Login Beta138 Situs judi resmi berlisensi

Khuy?n mai GK88: Nha cai uy tin Vi?t Nam – Slot game d?i thu?ng

Bandar togel resmi Indonesia: Abutogel – Bandar togel resmi Indonesia

Abutogel: Abutogel login – Abutogel

https://abutowin.icu/# Bandar togel resmi Indonesia

https://t.me/s/TgGo1WIN/20

Swerte99 online gaming Pilipinas: Swerte99 app – Swerte99 app

Slot jackpot terbesar Indonesia Situs judi online terpercaya Indonesia Slot jackpot terbesar Indonesia

Online betting Philippines: jollibet casino – jollibet login

Casino online GK88: Slot game d?i thu?ng – Ðang ký GK88

Swerte99 login: Swerte99 casino walang deposit bonus para sa Pinoy – Swerte99 casino walang deposit bonus para sa Pinoy

Online gambling platform Jollibet: Jollibet online sabong – jollibet app

Swerte99 slots: Swerte99 login – Swerte99 casino walang deposit bonus para sa Pinoy

Qeydiyyat bonusu Pinco casino Yeni az?rbaycan kazino sayt? Qeydiyyat bonusu Pinco casino

https://gkwinviet.company/# Khuy?n mai GK88

jollibet app: jollibet casino – Jollibet online sabong

jilwin: Jiliko – Jiliko

Cá cu?c tr?c tuy?n GK88: GK88 – Cá cu?c tr?c tuy?n GK88

Bandar togel resmi Indonesia Abutogel Bandar togel resmi Indonesia

Link alternatif Abutogel: Situs togel online terpercaya – Situs togel online terpercaya

Abutogel login: Abutogel – Abutogel

Online betting Philippines: Jollibet online sabong – Online gambling platform Jollibet

Pinco il? real pul qazan Canl? krupyerl? oyunlar Uduslar? tez c?xar Pinco il?

Promo slot gacor hari ini: Bonus new member 100% Beta138 – Slot gacor Beta138

https://betawinindo.top/# Promo slot gacor hari ini

Link alternatif Mandiribet: Mandiribet login – Judi online deposit pulsa

Slot game d?i thu?ng: Slot game d?i thu?ng – Cá cu?c tr?c tuy?n GK88

Swerte99 casino Swerte99 casino Swerte99

Abutogel login: Abutogel – Bandar togel resmi Indonesia

jollibet login: jollibet casino – jollibet

Khuy?n mai GK88: GK88 – Link vao GK88 m?i nh?t

Online casino Jollibet Philippines: Jollibet online sabong – jollibet login

Online gambling platform Jollibet: jollibet – Online betting Philippines

Khuy?n mai GK88 Casino online GK88 GK88

Withdraw cepat Beta138: Link alternatif Beta138 – Withdraw cepat Beta138

https://abutowin.icu/# Link alternatif Abutogel

1win: Ставки на спорт и киберспорт! Коэффициенты, бонусы и акции ждут тебя! Регистрируйся и выигрывай! https://t.me/s/Official_1win_kanal/3564 #1win #ставки #бонусы

1win: Ставки на спорт и киберспорт! Коэффициенты, бонусы и акции ждут тебя! Регистрируйся и выигрывай! https://t.me/s/Official_1win_kanal/4724 #1win #ставки #бонусы

Официальный Telegram канал 1win Casinо. Казинo и ставки от 1вин. Фриспины, актуальное зеркало официального сайта 1 win. Регистрируйся в ван вин, соверши вход в один вин, получай бонус используя промокод и начните играть на реальные деньги.

https://t.me/s/Official_1win_kanal/821

Mexican Pharmacy Hub: generic drugs mexican pharmacy – accutane mexico buy online

buy medicines online in india indian pharmacy buy medicines online in india

erythromycin online pharmacy: best online propecia pharmacy – MediDirect USA

generic drugs mexican pharmacy: Mexican Pharmacy Hub – Mexican Pharmacy Hub

https://t.me/s/Official_1win_kanal?before=6142

https://indianmedsone.shop/# Indian Meds One

Indian Meds One: best online pharmacy india – Indian Meds One

MediDirect USA: ketamine online pharmacy – online pharmacy buy viagra

Mexican Pharmacy Hub Mexican Pharmacy Hub buy cheap meds from a mexican pharmacy

top 10 pharmacies in india: best online pharmacy india – top 10 pharmacies in india

top 10 pharmacies in india: buy medicines online in india – top online pharmacy india

Indian Meds One: Indian Meds One – pharmacy website india

Mexican Pharmacy Hub: semaglutide mexico price – gabapentin mexican pharmacy

indian pharmacies safe reputable indian online pharmacy best india pharmacy

http://mexicanpharmacyhub.com/# Mexican Pharmacy Hub

tri luma online pharmacy: MediDirect USA – MediDirect USA

Indian Meds One: pharmacy website india – world pharmacy india

legit mexican pharmacy for hair loss pills: Mexican Pharmacy Hub – get viagra without prescription from mexico

Indian Meds One: indian pharmacy online – india online pharmacy

MediDirect USA fluconazole target pharmacy MediDirect USA

Indian Meds One: reputable indian pharmacies – online pharmacy india

mexican pharmaceuticals online: Mexican Pharmacy Hub – mexico pharmacies prescription drugs

https://replit.com/@jwypjhmjedpapqd cenforce dapoxetine

https://mexicanpharmacyhub.shop/# Mexican Pharmacy Hub

Mexican Pharmacy Hub: Mexican Pharmacy Hub – Mexican Pharmacy Hub

Mexican Pharmacy Hub: cheap mexican pharmacy – Mexican Pharmacy Hub

cheapest online pharmacy india: pharmacy website india – Indian Meds One